When I was first in practice, the only way to gain “small entity” status as a US patent filer was by filing a “small entity status form”. It was thus a pretty big deal in the year 2000 when the USPTO published a Federal Register notice (65 FR 54603, September 8, 2000) which pretty much eliminated the need for small entity status forms. Oversimplifying slightly, starting on November 7, 2000, a patent applicant in the USPTO was able to gain small entity status by the simple step of paying a government fee at the small entity rate. Except not! PCT filers sometimes find to their great disappointment that is is not really true that you can always gain gain small entity status by the simple step of paying a government fee at the small entity rate.

The first thing that we need to do is make sure that we realize how short the list is of the government fees that actually do count as small entity assertions when they are paid. This short list, defined in 37 CFR § 1.27(c)(3), is as follows:

-

- fee code 2011 — Basic filing fee – Utility

- fee code 4011 — Basic filing fee – Utility – electronic

- fee code 2012 — Basic filing fee – Design

- fee code 2017 — Basic filing fee – Design CPA

- fee code 2013 — Basic filing fee – Plant

- fee code 2005 — Provisional application filing fee

- fee code 2014 — Basic filing fee – Reissue

- fee code 2019 — Basic filing fee – Reissue (Design CPA)

- fee code 2601 — PCT Transmittal fee

- ISA/US small entity search fee paid in exact amount to an RO other than RO/US

- fee code 2631— Basic national stage fee

- small entity first part of the Hague individual designation fee for the United States to the International Bureau

That’s it. Only twelve fees. If one of these twelve small entity fees is paid in a particular application, then this gives the applicant a free pass on having to file a “small entity” form in that application to gain small entity status. Otherwise, if an applicant wishes to gain small entity status in a particular application, the applicant will need to file a small entity form.

So now let’s focus on the filing of a PCT application and in particular let’s focus on the events that might occur during the international phase. We can observe immediately that the filer of a PCT application is never going to be paying any of fees 1 through 8 during the international phase of a PCT application. The filer might pay fee 11 when entering the US national phase, but right now I am focusing on the international phase, so fee 11 is not relevant to the present discussion. Fee 12 relates only to Hague applications (international design applications), so fee 12 is not relevant to the present discussion. So all that remains to discuss here is fees 9 and 10.

Fee 9. The only way that you as a PCT filer would be paying fee 9 is if you happen to have selected RO/US as your Receiving Office. If you did select RO/US as your RO, and if you specifically paid fee code 2601 (the small entity transmittal fee) then you will have established small entity status for purposes of the USPTO. This small entity status will persist through the international search process (which would be relevant only if the ISA that you selected happened to be ISA/US) and through the international preliminary examination process (which would be relevant only if you were to choose to file a Demand, and then only if the IPEA that you selected happened to be IPEA/US) and it will persist through the entry into the US national phase and through the prosecution of the 371 application. The applicant who has paid fee code 2601 will get a free pass on having to file a small entity status form. If for example the applicant were to choose to file a Demand, the applicant would be entitled to pay the small entity fee for the IPEA/US preliminary examination fee.

Fee 10. Now let’s suppose that the RO that you selected happened not to be the RO/US. The interesting question would be which ISA you happened to choose for filing this new PCT application in that RO. If the ISA that you chose happened to be ISA/US, and if the search fee that you paid to the RO (which again, we emphasize, is an RO that is not the RO/US) happened to be exactly the small-entity fee for the ISA/US under PCT Rule 16, then this will count as an assertion of small entity status. This small entity status will persist through the international search process (which we understand will take place at the ISA/US, since that is the ISA that you chose) and through the international preliminary examination process (which would be relevant only if you were to choose to file a Demand, and then only if the IPEA that you selected happened to be IPEA/US) and it will persist through the entry into the US national phase and through the prosecution of the 371 application. The applicant will get a free pass on having to file a small entity status form because the applicant paid the exact ISA/US search fee to an RO that was not the RO/US. If for example the applicant were to choose to file a Demand, the applicant would be entitled to pay the small entity fee for the IPEA/US preliminary examination fee.

Now we can identify the traps for the unwary PCT filer.

One trap for the unwary PCT filer would be the PCT filer who filed in RO/US but who for some reason did not think to assert small entity status at the time of paying the transmittal fee to the RO/US. Such a PCT filer might at some later time in the international phase suddenly get the idea of wanting to get away with paying small entity fees. An example of this could be the filer that had chosen ISA/US and was invited to pay additional fees to the ISA (because of a lack of unity of invention) and suddenly realized that the additional fees would add up to a lot of money, and belatedly realized that the applicant did qualify for small entity status. The filer might mistakenly assume that nothing more is required to gain small entity status than the mere payment of small entity fees to the ISA/US. But this is not so! The real situation is that the filer is going to have to file a small entity status form to gain small entity status.

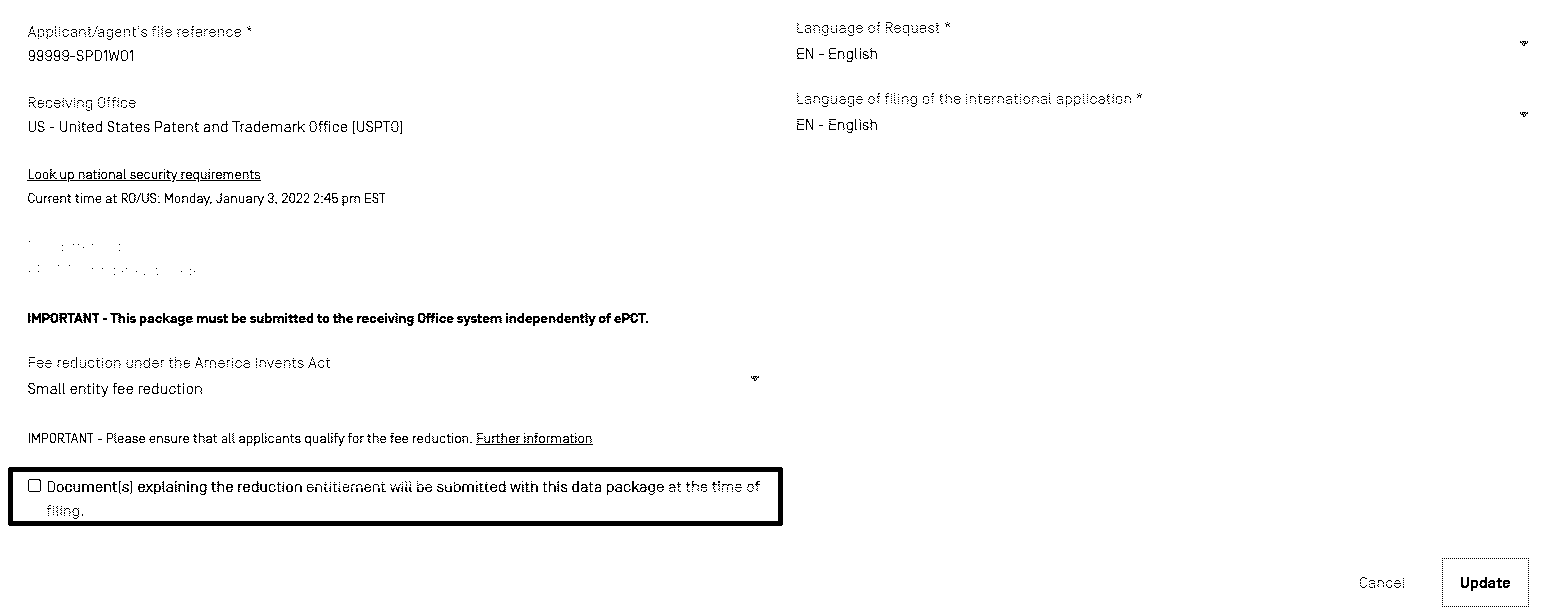

This is the purpose of the check box in the ePCT form that you see above. The check box and its accompanying language might help the filer to recognize the need to file the small entity status form. The filer might wish to check that box in ePCT and provide a small entity status form.

But of course the PCT filer who filed in RO/US is unlikely to use ePCT for anything about responding to the invitation to pay additional fees. The same factors that prompted the filer to pick RO/US as the RO are likely to prompt the filer to pick either EFS-Web or Patentcenter for the response, in which case the filer would not encounter that check box in ePCT. But the filer would still be in a situation where the mere payment of a small entity fee to the ISA/US is not going to suffice as a way to gain small entity status. It would still be necessary to file a small entity status form to gain small entity status. Neither EFS-Web nor Patentcenter, however, offers this helpful reminder the way that ePCT does. It is up to the filer to somehow realize that there is the need to provide the small entity status form.

A variant of this trap is the PCT filer that filed in RO/US but who for some reason did not think to assert small entity status at the time of paying the transmittal fee to the RO/US, and whose belated desire to gain small entity status did not arise until the time came to file a Demand (and this assumes the filer had consciously selected IPEA/US as the IPEA for the Demand). If the filer happened to be filing the Demand by means of ePCT, then the filer’s encountering this check box in ePCT might serve as a reminder of the need to file a small entity status form. But the same factors that prompted the filer to choose RO/US as the RO would very likely prompt the filer to choose EFS-Web or Patentcenter as the filing path for the Demand. Again, as mentioned above, neither EFS-Web nor Patentcenter provides any reminder of the need to file a small entity status form. It is up to the filer to somehow realize that the form is needed.

Now consider the filer who did not previously establish small entity status, and that is using ePCT to file a Demand. (A typical way that this might arise is that the filer is located outside of the US.) And suppose the filer has selected IPEA/US as the IPEA for the Demand. And suppose further that the filer wants to pay merely the small entity fee to the IPEA/US. The trap for the unwary is that the mere payment of the small entity fee will not serve as an assertion of small entity status. It will be necessary for the filer to provide a small entity status form. Fortunately ePCT provides the check box, and this might serve as a reminder to the filer to provide that form.

Now we can turn to what might be the most subtle of the traps for the unwary in all of the fact patterns that might be devised for the international phase of a PCT application. We start with a general question. What happens when a filer makes a mistake and sends a document to the wrong Office? For example, suppose there is some document that the filer was supposed to send to the International Bureau, and the filer made the mistake of sending it to a Receiving Office? It turns out that there are PCT procedures that provide for this. In general, any PCT Office is supposed to look at any document that it receives and if that Office is not competent to handle the document, that Office is supposed to forward the document to whichever Office is the correct Office. (It might take days or weeks for the document to reach that correct Office, and by then the due date for the arrival of the document might have come and gone, but that is another matter.)

But there is a particularly subtle trap lurking in this PCT procedure, and it relates to the filing of Demands. Consider the PCT filer that decides to file a Demand, and that chooses an IPEA that is not the IPEA/US. And suppose further that this filer is located in the US. This filer might be tempted to try to use EFS-Web or Patentcenter as the way to file that Demand, for no better reason than that EFS-Web and Patentcenter are perhaps very familiar to that US-based filer as ways of doing e-filing generally. What the filer might think is that the USPTO, after receiving that Demand, would forward it on to the filer’s chosen IPEA. This is not, however, what would happen. The reason why this would not happen is that the IPEA/US is a “universal acceptor”. Just as someone with AB+ blood can receive a blood donation from anybody with anybody of the other blood types, so will IPEA/US accept the task of doing an international preliminary examination no matter which ISA the applicant had previously selected. This means that the USPTO as an IPEA will be “competent” and thus feels no need to forward the Demand to any other Office due to any lack of competence. This also means that the filer will not actually get to make use of the IPEA that the file actually selected.

And, as it relates to this blog article, if the filer had not previously done what was needed to secure small entity status, and if the filer now wished to get away with only having to pay the small entity fee to the IPEA/US, then it would not be sufficient to merely pay the small-entity fee. The filer would need to hand in the small entity status form. Again, neither EFS-Web nor Patentcenter will provide any reminder about this.

How, by the way, does the filer avoid this particular trap? This particular trap for the unwary is avoided by making use of ePCT rather than EFS-Web or Patentcenter as the way to e-file the Demand. With ePCT, the filer is essentially entrusting to the IB the task of forwarding the Demand to the IPEA of the filer’s choice.

How exactly does one secure “small entity status” before the USPTO? Where may one find this all-important “small entity status form”?

When I was first in practice, the USPTO provided a small entity status form. It was form PTO/SB/10. That form is no longer available on the USPTO web site but you can see it here. 37 CFR § 1.27(c)(1) makes clear that you can actually make up your own small entity status form in a word processor. Here is what the rule says:

Small entity status may be established by a written assertion of entitlement to small entity status. A written assertion must:

(i) Be clearly identifiable;

(ii) Be signed … ; and

(iii) Convey the concept of entitlement to small entity status, such as by stating that applicant is a small entity, or that small entity status is entitled to be asserted for the application or patent. While no specific words or wording are required to assert small entity status, the intent to assert small entity status must be clearly indicated in order to comply with the assertion requirement.

It strikes me that an easy way to do this would be to say “Applicant is entitled to assert small entity status for this application.” and put a signature next to those five words.

One more thing strikes me about all of this. It seems to me that what the USPTO ought to do is eliminate most of these traps for the unwary. The USPTO already apparently seems to think that it is okay for a PCT filer located outside of the US, who is making use of a Receiving Office that is located outside of the US, to assert small entity status by the mere payment of a search fee to the ISA/US that matches exactly the small entity search amount. So the USPTO ought to amend 37 CFR § 1.27(c)(3) so that each of the “trap” fees would also count as an assertion of small entity status. This includes the following:

-

- payment of additional-invention fees to the ISA/US at the small entity rate in response to an invitation to pay additional fees,

- payment of a preliminary examination fee to the IPEA/US at the small entity rate, and

- payment of additional-invention fees to the IPEA/US at the small entity rate in response to an invitation to pay additional fees.

Such an amendment to 37 CFR § 1.27(c)(3) would save lots of work for USPTO personnel who, under present circumstances, are forced to go back and forth with PCT filers every time a filer steps into one of these traps and has to either cobble together a small entity form or fuss around with payment of a deficiency amount for a fee. It would also save trouble and delay for the filer.

I’ve come across another situation where one has to provide a “small entity declaration”: filing in the RO/IL but choosing ISA/US claiming small entity for the search fee. The RO/IL requests a ‘declaration’ which can be in the form of a one-sentence-letter, but needs to be signed (preferably by the applicant, but if not possible, they’ll also accept agent’s signature.

When this arises, are you using ePCT or some other filing mechanism?

Personally, I only use ePCT, nothing else (not since we started using it many years ago). I just ran a quick test, ePCT prompts you to attach a declaration when choosing ISA/US in a RO/IL or RO/IB case. I do not know when this prompt was added, or if has been there all the time. But it’s not a mandatory document without which one could not file.

I have had cases, though, filed by other people, not paying attention to the prompt, and the RO/IL simply called and asked us to submit.

What a brilliant way to operate a patent office: Something is missing? Simply call applicant’s representative and ask them to send it in.

Miracles do happen …

While simply stating that “Applicant is a small entity” would appear to conform to 37 CFR 1.27(c)(1)(iii), it is important to keep in mind that small entity status is invention-specific. A company of fewer than 500 employees is a small entity with respect to an invention that has not been licensed, but is not a small entity with respect to an invention that has been licensed to a “large” company (one with more than 500 employees).

To serve a reminder function (to both the practitioner and the client), it might be preferable to use a longer phrase, such as: “Applicant is entitled to assert small entity status for this application.”

You are right about all of this. I blogged about this here.

I read the post at the time, but had forgotten about it. Thanks! In any case, I had no doubt that the reminder function would be surplusage for you. Others might benefit…

Not just “licensed”, but any one of licensed, assigned, and under a contract or obligation to license or assign the application. Any of those conditions will remove entitlement to small entity status.

Absolutely right, Rick. I should have been more complete in my post. Thanks!

You stated: “Otherwise, if an applicant wishes to gain small entity status in a particular application, the applicant will need to file a small entity form.”

I recognize that this post is about PCT applications but wanted to note something about U.S. national applications just in case I am missing anything. I believe that the “small entity form” usually used for US national applications would be the ADS. I acknowledge the continued existence of the provisional cover sheet, which I haven’t used in a decade. For a national phase, the PTO-1390 also has a small entity checkbox, but I can’t think of a situation where you wouldn’t still submit an ADS.

By checking the “Small Entity Status Claimed” checkbox on the ADS (which is signed by the practitioner), the USPTO assigns small entity status to the application, even if no fees are paid at filing. This leads me to believe that the ADS qualifies as the “small entity form” – or, in the language of 37 CFR 1.27(c)(1), the “Assertion by writing.” Agreed?

Hello.

Will USPTO still accepted a completed form of the PTO/SB/10 or do I really have to compose a letter version of it?